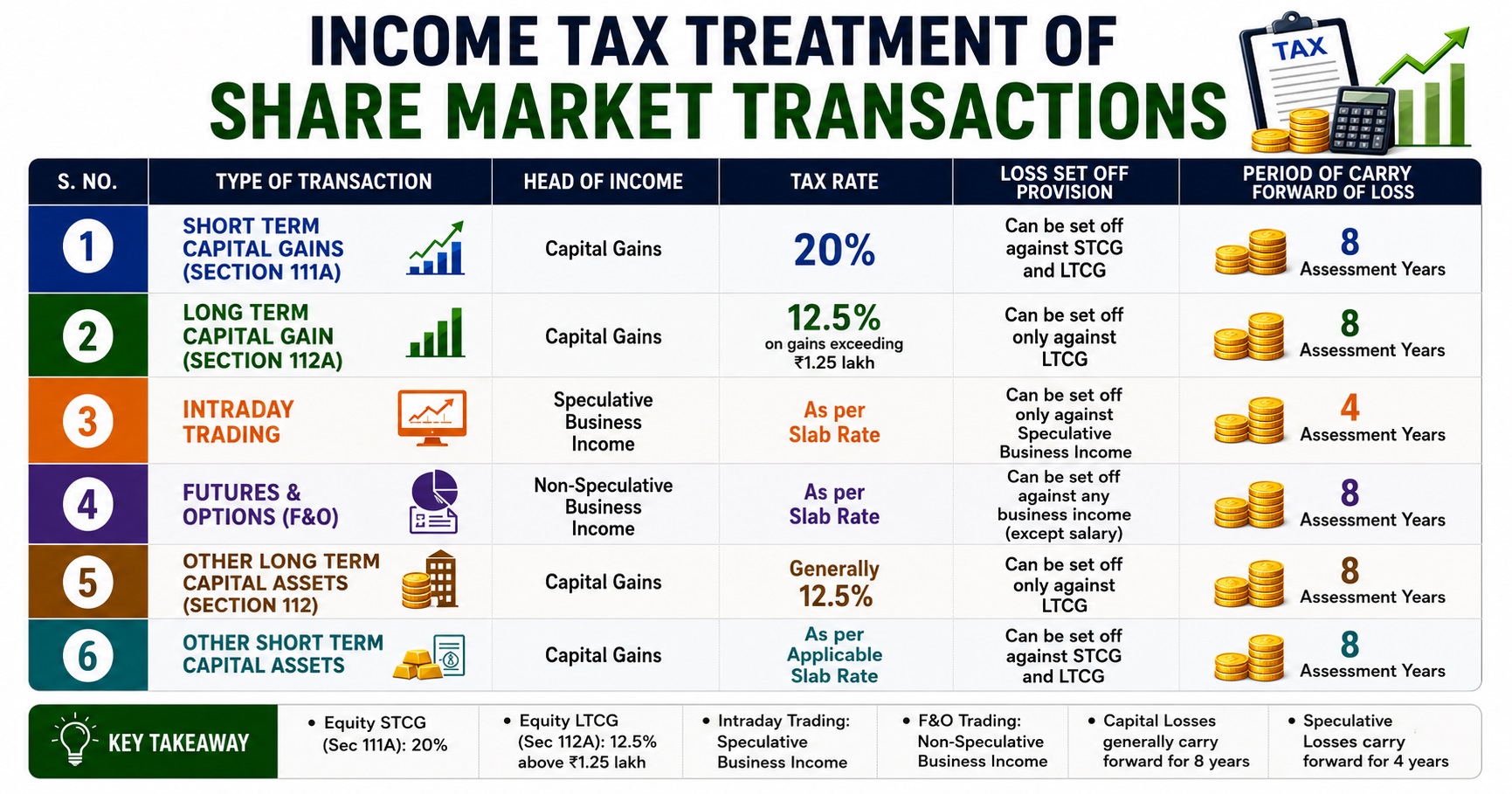

Share Market Taxation in India: STCG, LTCG, Intraday & F&O Tax Rules Explained

Understanding the taxation of different types of share market transactions is essential for every investor and trader. Tax treatment varies depending on whether you invest, trade intraday, or deal in Futures & Options (F&O). Knowing these rules can help you plan your investments more effectively and avoid surprises during tax filing.

1. Short-Term Capital Gain (STCG) – Section 111A

Short-Term Capital Gain arises when listed equity shares or equity-oriented mutual funds are sold within the prescribed holding period.

- Head of Income: Capital Gains

- Tax Rate: 20%

- Loss Set-Off: Can be set off against both STCG and LTCG

- Carry Forward of Loss: 8 Assessment Years

2. Long-Term Capital Gain (LTCG) – Section 112A

Long-Term Capital Gain applies when listed equity shares and equity-oriented mutual funds are held for the long term before being sold.

- Head of Income: Capital Gains

- Tax Rate: 12.5% on gains exceeding ₹1.25 lakh

- Loss Set-Off: Can be set off only against LTCG

- Carry Forward of Loss: 8 Assessment Years

3. Intraday Trading

Intraday trading refers to buying and selling shares on the same trading day without taking delivery.

- Head of Income: Speculative Business Income

- Tax Rate: As per Income Tax Slab Rates

- Loss Set-Off: Can be set off only against Speculative Business Income

- Carry Forward of Loss: 4 Assessment Years

4. Futures & Options (F&O) Trading

Income from Futures and Options trading is treated differently from intraday equity trading.

- Head of Income: Non-Speculative Business Income

- Tax Rate: As per Income Tax Slab Rates

- Loss Set-Off: Can be set off against any business income (except salary)

- Carry Forward of Loss: 8 Assessment Years

5. Other Long-Term Capital Assets – Section 112

This category includes assets such as land, buildings, debt mutual funds (where applicable), and unlisted securities.

- Head of Income: Capital Gains

- Tax Rate: Generally 12.5%

- Loss Set-Off: Can be set off only against LTCG

- Carry Forward of Loss: 8 Assessment Years

6. Other Short-Term Capital Assets

This category covers assets such as land, building, gold, debt investments, and other capital assets sold within the short-term holding period.

- Head of Income: Capital Gains

- Tax Rate: As per applicable Slab Rate

- Loss Set-Off: Can be set off against STCG and LTCG

- Carry Forward of Loss: 8 Assessment Years

Key Takeaway

Taxation plays a crucial role in determining your actual returns from investing and trading. Before making investment decisions, always consider the tax implications, loss adjustment rules, and carry-forward benefits available under the Income Tax Act.

A well-planned tax strategy can help you maximize returns, reduce tax liability, and manage your portfolio more efficiently.

Disclaimer: The above information is for educational purposes only. Tax laws are subject to change. Please consult your Chartered Accountant or tax advisor before making investment decisions.

No comments yet. Be the first to share your thoughts!

You must be logged in to write a comment.

Log In to Comment